End-of-line & warehousing packaging machinery market set to nearly double by 2029, says Vanessa Lopez.

The packaging machinery market in end-of-line and warehouse applications is one of the fastest-growing segments of the broader packaging industry, outpacing many traditional machinery markets. Major retailer Amazon has already taken note, announcing large-scale adoption of right-fit packaging solutions across its European operations. Moves like this underscore how regulatory pressures, labour costs, and the continued rise of e-commerce are reshaping investment priorities in both manufacturing and warehousing.

Interact Analysis’s new report, EoL & Warehouse Packaging Automation, examines this dynamic cross-section, covering equipment ranging from case erectors and palletizers to emerging right-fit systems and automated baggers. The report sizes and forecasts the fast-growing market, highlighting the key trends driving automation forward. Below are high-level findings and analysis from the report.

average earnings climbed, creating an

expanding labour gap

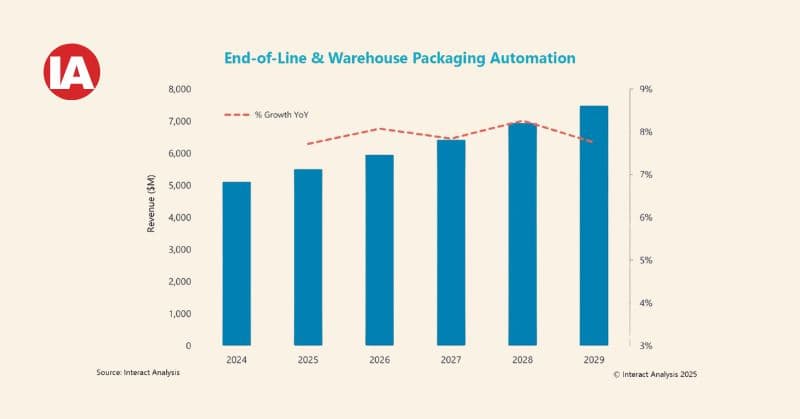

Market overview

Within end-of-line and warehousing applications, the packaging machinery market is set for strong expansion, with forecast growth from $5.1 billion in 2024 to nearly $7.5 billion by 2029; a compound annual growth rate (CAGR) of 7.9%. The drivers behind this growth are consistent across regions: rising labour costs, regulatory pressure on packaging materials, and the accelerating role played by e-commerce in shaping how products are packed and shipped.

Three key factors impacting the market

1. Regulatory pressures

Sustainability and regulation are becoming central to packaging machinery decisions. In Europe, the Packaging and Packaging Waste Regulation (PPWR) is setting strict requirements that go beyond recyclability targets. A key provision requires that e-commerce packages be at least 50% full, with major reductions in excess packaging mandated. Companies that fail to comply face fines.

In the US, state-level Extended Producer Responsibility (EPR) laws are creating similar compliance burdens. Producers in states such as Maine, Oregon, and Colorado are required to track and report packaging material use, with financial penalties for non-compliance. For companies operating across both the EU and the US, this creates a complex regulatory environment that demands new approaches to packaging efficiency and material usage.

These policies fuel demand for right-fit packaging solutions – which minimize void fill, reduce package dimensions, and provide traceable data on material usage – to support reporting requirements. Only a few players serve this market today. Up until recently, the most notable were CMC Technologies, Packsize and Sparck Technologies. However, Packsize recently announced its intention to acquire Sparck Technologies, further consolidating the market. Despite the limited vendor base, large retailers like Amazon have already made major investments in these systems. Amazon has announced it will deploy more than 70 right-fit boxing solutions across Europe over the next few years.

2. Labour costs

Rising labour costs are one of the strongest forces shaping investment in packaging machinery today. In regions such as the Americas and Europe, wage growth and worker shortages are pushing companies to adopt automation to reduce operating expenses and maintain throughput. In the US, for example, manufacturing employment has decreased while wages continue to rise, creating a widening gap between labour availability and labour cost, as shown in the chart below.

This widening labour gap is accelerating investment in automation, particularly in areas like palletizing, where robotic systems are beginning to outpace conventional machinery adoption. Compared with conventional high-speed palletizers, robotic arms are easier to reprogram, require less maintenance, and can be adapted for a wider range of products. For many operators, this flexibility makes them not only a labour-saving investment but also a more sustainable long-term choice.

proportion of US retail sales since the Covid-19 pandemic

3. E-commerce

By mid-2025, e-commerce accounted for 16.3% of total US retail sales, matching the peak level reached during the pandemic in 2020. The difference this time is that the share has held steady under very different conditions, signaling that online retail has become a permanent feature of the US consumer landscape. As shown in the chart below, e-commerce penetration has stabilized at a structurally higher level, keeping pressure on fulfillment operations to move goods quickly and efficiently.

Walmart made early investments in right-fit solutions through its 2023 partnership with Packsize, focusing on its grocery fulfillment centers. While this initial rollout was limited, the move set an important precedent. As competition with Amazon intensifies, Walmart could expand automation more broadly across its fulfillment network, using right-fit systems to keep pace with growing demand for speed, cost, and efficiency.

Although adoption of right-fit packaging is still at an early stage, the implications for fulfillment centers are significant. Unlike manufacturing lines, warehouses must handle a constantly shifting mix of SKUs and order sizes, making flexible solutions like right-fit packaging especially valuable.

Looking ahead

Packaging machinery used in end-of-line production and warehousing is on track to nearly double in value between 2024 and 2029, making it one of the fastest-growing segments of the broader packaging industry. This growth reflects not only regulatory and labour pressures, but also the rapid rise of e-commerce and the demand for more efficient fulfillment operations.

The market is also being reshaped by a wave of partnerships. Walmart’s 2023 collaboration with Packsize signaled the first step toward right-fit automation in its fulfillment operations. Amazon followed with one of the largest coordinated rollouts of right-fit packaging in Europe, underscoring the technology’s strategic value. And most recently, Packsize joined forces with Bastian Solutions, embedding right-fit systems within broader warehouse automation projects.

Together, these moves underscore the momentum behind packaging automation adoption, the accelerating race between retailers to become the industry leader, and the competitive opportunities emerging in this space. This first edition of Interact Analysis’s report establishes the baseline for a fast-moving market, providing the insight needed to navigate its growth trajectory.

The EoL and Warehouse Packaging Automation report is now available from Interact Analysis. For more information, contact [email protected].

Vanessa Lopez, Market Analyst at Interact Analysis, specialises in industrial automation and packaging machinery. With a strong quantitative and qualitative research background, Vanessa contributes valuable insights to strategic initiatives. She holds a bachelor's in Psychology and a master's in Communication from the University of Texas at Austin. Vanessa is based in the US office.

Author